Logistics real estate is increasingly exposed to physical climate change risks.

Extreme weather events and rising sea levels threaten locations, supply chains and infrastructures. At the same time, growing regulatory and market pressures force banks, insurance companies and investors to make climate resilience an integral part of their site and investment criteria.

Due to its dependence on functioning transport networks and infrastructures, the logistics industry is exposed to the consequences of climate change more than others. Extreme weather events like storms, heavy rain, floods and heat waves affect access routes, storage facilities and transshipment infrastructure while also disrupting supply chains and increasing maintenance costs. The damage wrought by natural disasters is going up steadily and can no longer be ignored (see Figure 1). Surveys have revealed: Two out of three companies already noted resource shortages and disrupted supply chains, with one in two reporting damages to buildings and roads – which means that physical climate risks represent a pressing operational issue.[1]

Just how severely logistics real estate is affected depends chiefly on a given site and its layout. Intense soil sealing aggravates the risks of flooding and heat while municipal governments increasingly prescribe climate-adjusted planning and construction via their local development plans. At the same time, short-sighted business logic and high capital expenditure requirements tend to impede proactively implemented mitigation measures. Instead, such measures are often delayed until insurance companies, banks or authorities explicitly demand them.

Note: During the first half of 2025, natural disasters caused c. USD131 billion worth of damage – of which 60% was not covered by insurance.

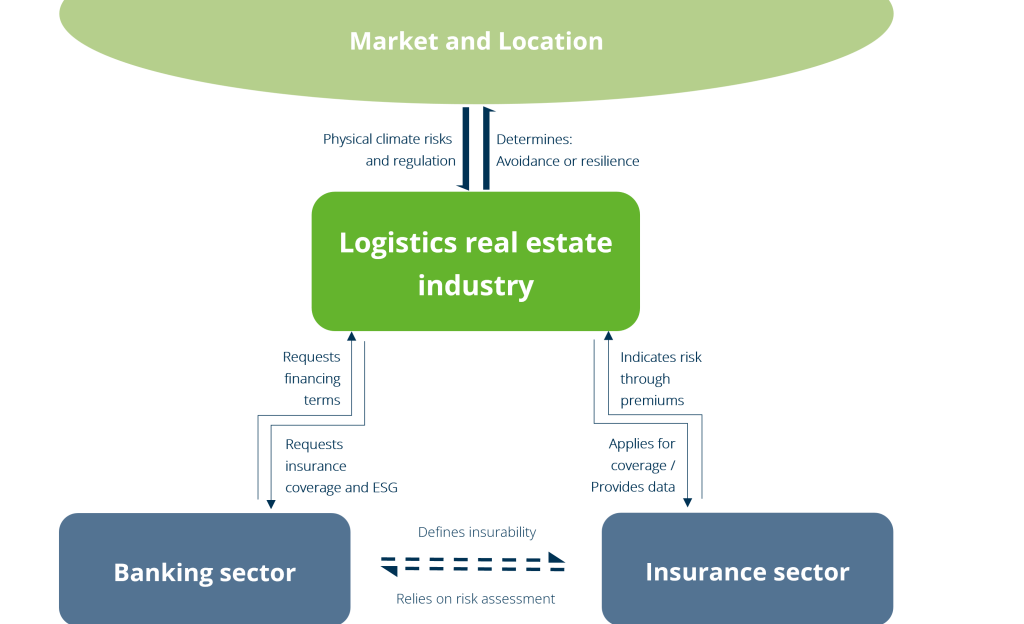

In light of the growing damage caused by climate change, risk ownership among the real estate sector, insurance companies and banks is shifting (see Figure 2). For assets in particularly exposed locations, the threat of being rated as difficult or impossible to insure is becoming a reality – with direct consequences for their funding eligibility, profitability and fungibility. Insurance companies are responding to elevated damage amounts and vague forecasts by raising premiums, tightening conditions, increasing deductibles and, in extreme cases, by pulling out of high-risk regions.

For banks, physical climate risks have evolved from a secondary long-term issue into a factor clearly relevant in their underwriting practice. Site exposure, structural resilience and insurability are moving into focus alongside the traditional credit rating metrics. This may lead to more restrictive conditions, higher capital adequacy requirements or the outright rejection of projects in high-risk locations. At the same time, the dovetailing of financing and insurance—for instance through insurance coverage requirements and risk transfer to the capital market—further increases the complexity of risk distribution while making transparency in climate risk management one of the decisive competitive factors.

Regulatory specifications increase the pressure to manage climate risks in a structured manner. Insurance companies are calling for climate-adjusted planning, construction and refurbishment, a construction ban in high-risk flood areas and compulsory climate risk assessments, whereas supervisory authorities expect banks to integrate climate-related threats in their risk and capital planning. Most institutes have by now added physical risks to their stress tests, and yet data gaps and uncertain assessment aspects remain.

For the real estate industry, systematic climate change mitigation strategies are becoming the precondition for stable business models. Central instruments include vulnerability analyses that rate the exposure, sensitivity and adaptability of a given site, and their findings are used as basis for investment decisions, property strategies and redevelopment planning. They provide transparency in regard to risky assets and resilient sites – and are therefore equally useful to banks, investors and insurance companies as they adapt their terms, capital allocation and portfolio management to climate risks.

GARBE takes climate change risks into account within the scope of its ESG activities, and started commissioning third-party climate risk analyses for its assets years ago. These analyses are firmly integrated into our ESG software: For any asset managed by GARBE, a site-specific climate risk assessment can be generated which may then be used to identify potential risks and to review possible mitigation measures. This way, the portfolio management stays up to date on climate-related opportunities and risks.

At the same time, GARBE keeps in touch with insurance and finance partners to recognise market dynamics such as premiums, conditions and regulatory requirements as soon as they emerge, and to ensure that the strategy takes them into account. The approach is complemented by the company’s adherence to leading ESG benchmarks such as GRESB, which communicates the progress made in climate risk management to the outside world.

Climate change risks are rapidly gaining in significance for the logistics real estate sector and increasingly influence aspects like site selection, asset strategy, insurability and financing. Extreme weather, potentially higher upkeep costs and tighter regulations could heighten the risk of damage, impairments and rent discounts.

For owners, developers, investors, insurers and banks, this means: Climate resilience should be integrated in a data-driven and site-specific form into the planning, approval, funding and operation of logistics real estate early on. Taking an integrative approach that consistently synchronises site-specific exposure, structural adaptability, insurability and regulatory requirements will enable you to contain your risks and simultaneously to seize opportunities, e.g. in the form of better financing conditions and a superior position when competing for tenants, capital and land.

We use cookies on our site. Some of them are essential, while others help us to improve this website and to show you personalised advertising. You can either accept all or only essential cookies. To find out more, read our privacy policy and cookie policy. If you are under 16 and wish to give consent to optional services, you must ask your legal guardians for permission. We use cookies and other technologies on our website. Some of them are essential, while others help us to improve this website and your experience. Personal data may be processed (e.g. IP addresses), for example for personalized ads and content or ad and content measurement. You can find more information about the use of your data in our privacy policy. You can revoke or adjust your selection at any time under Settings.

If you are under 16 and wish to give consent to optional services, you must ask your legal guardians for permission. We use cookies and other technologies on our website. Some of them are essential, while others help us to improve this website and your experience. Personal data may be processed (e.g. IP addresses), for example for personalized ads and content or ad and content measurement. You can find more information about the use of your data in our privacy policy. This is an overview of all cookies used on this website. You can either accept all categories at once or make a selection of cookies.